Liquid Staking Derivatives & The Shanghai Upgrade

Liquid Staking Derivatives & The Shanghai Upgrade

Who Will Be Crowned The "Winner" of Liquid Staking?

Liquid Staking Derivatives (LSDs) have been the center of attention to start off 2023. The Shanghai Upgrade is planned for late March 2023, which means we can expect a lot of previously locked ETH to come back online. Users have a lot of options to pick from. Despite the protocols all solving the same problem, they all offer something a bit different. The continued debate is about who will be the “winner” post-Shanghai. I think of this scenario a lot like the Curve Wars. There is no “winner” per se, but it’s a game of who can take that top TVL spot and hold on to it. Lido has dominated the liquid staking space since the very beginning, but can the Shanghai upgrade break their once untouchable monopoly?

Current Landscape:

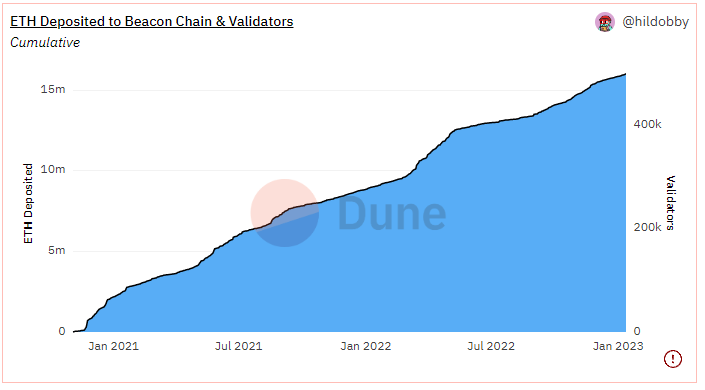

Currently, there is 16m ETH ($25b USD) deposited to Beacon Chain. Its been a steady climb up in deposits ever since Beacon Chain went live on December 1st, 2020. The issue with Beacon Chain at scale was that you needed 32 ETH in order to run a validator. At the time, 32 ETH was about $20k USD. This weeded out a lot of potential retail/smaller investors who were interested in participating, but couldn’t afford to lock away $20k USD for an unknown period of time. Nobody likes their money being locked away with no option to get it back. A few weeks after Beacon Chain went live, we were introduced to Lido Finance which offered liquidity for staked ETH. The beauty of Lido Finance was that you could deposit any amount of ETH, you were entitled to the yield generated proportionate to what you staked, and it was also liquid. Liquidity was the biggest driver. With Lido, you would stake your ETH and receive what they called stETH (Staked ETH) and it accrued rewards in real-time, while you could use the stETH across DeFi to do whatever you wanted with it. If you wanted out? No problem, stETH liquidity was available across various dex’s.

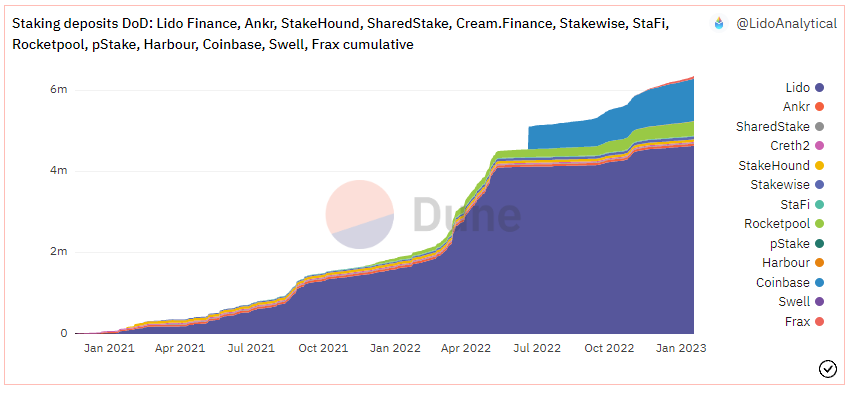

Since Lido was the first to market, they got the first-mover advantage. They currently have 29% market share of all ETH deposits on Beacon Chain. That represents 4.64m ETH of the 16m ETH total deposited, or $7.28b of the total $25b USD.

Note, this is for all ETH deposits, not just Liquid Staking Derivatives

As the years went on, many entered the game of liquid staking as they saw the sheer amount of TVL you could amass whilst taking a small fee during the process. The five I’m focusing on are Lido Finance, Rocket Pool, Frax Finance, Stakewise, and Coinbase. I chose these five as they appear to be the most popular of the bunch and I can see them all succeeding in one way or another over the course of this year.

Here’s a quick overview of where we stand as of January 17th, 2023. As we all know, Lido ($LDO) has a first-mover advantage and is leading the way by more than 4x on Coinbase. Lido launched stETH in December 2020, 2 weeks after the Beacon Chain launch. Coinbase ($COIN) launched cbETH in June of 2022, however being one of the largest exchanges, their ability to accrue ETH has been easier than smaller DeFi protocols. They custody 18m ETH, have over 100m users, and with a simple UI/UX on any available smartphone…you can imagine it’s fairly easy for them to gain traction. RocketPool ($RPL) launched rETH in October of 2021 and has been a clear 2nd place in terms of DeFi LSDs. Stakewise ($SWISE) launched sETH2 in February of 2021. Frax Finance ($FXS) launched frxETH in October of 2022 and has been absolutely killing it on TVL growth.

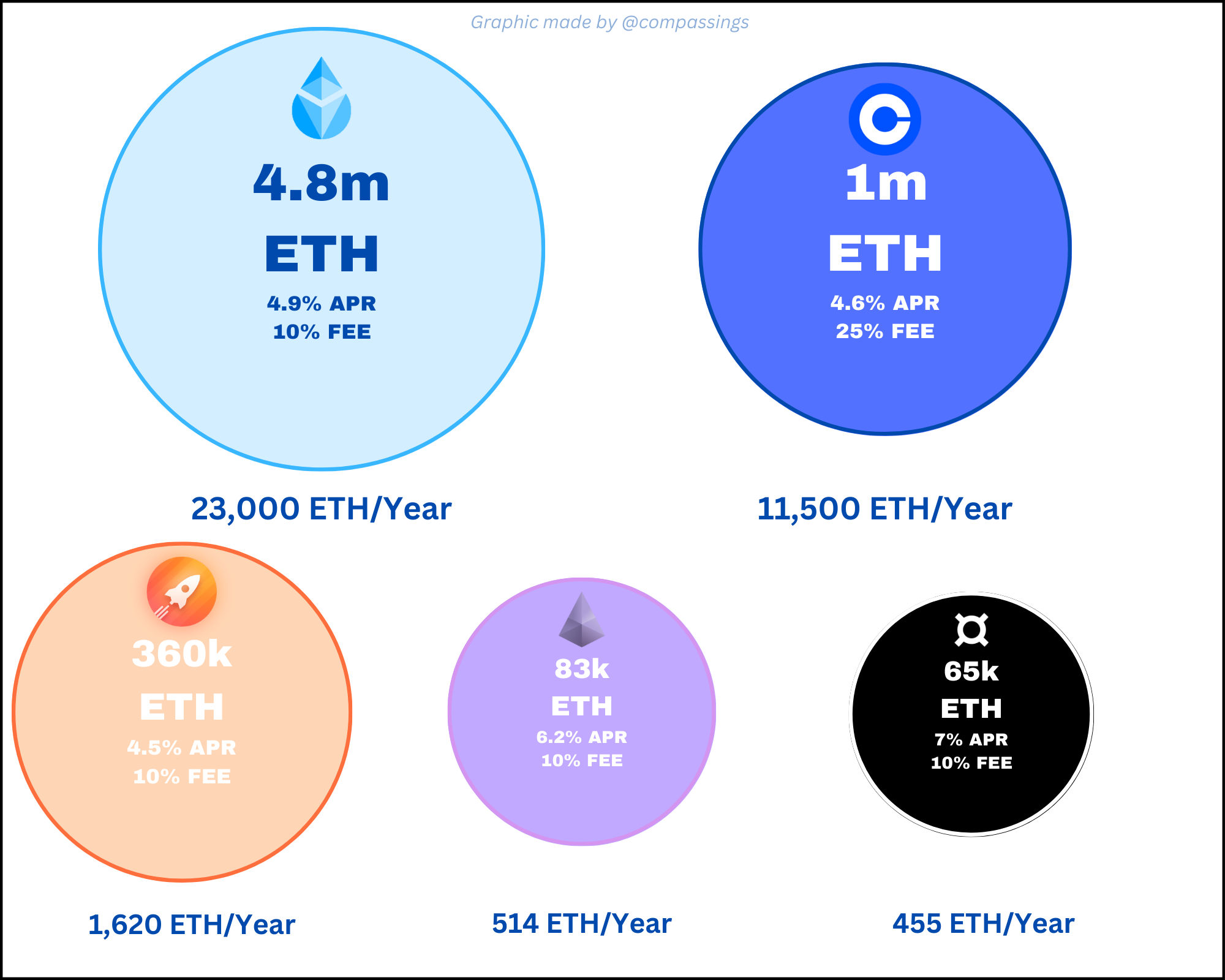

As we can see, Lido is generating an enormous amount of fees every year. Taking current ETH prices into account, that’s about $34.5m in fees. Coinbase charges 2.5x the amount Lido does, and makes close to $17.5m a year in fees. RocketPool makes $2.43m, Stakewise makes $770k, and Frax makes $682k.

These are bound to change dramatically in the coming months, and even change on a daily basis. This graphic is more for a general idea of what they are making at current levels if they were to stop accepting deposits at this very moment.

Shanghai Upgrade:

The next milestone in Ethereum’s roadmap is the Shanghai upgrade, which enables withdrawals from ETH Validators from the Beacon Chain. The Beacon Chain launched on December 1st, 2020. This means that stakers who originally staked their 32 ETH per validator will be able to gain liquidity back after almost 2 and a half years. The ultimate goal with shanghai is to continue enhancing the scalability of Ethereum. However, once Shanghai goes live, not all the ETH becomes immediately withdrawable. Ethereum is dynamically based on how many validators are exiting at a given time.

The Validators have to go through two stages. The first stage is the exit queue which is defined by the following variables.

The full number of validators,

The minimum churn limit (4)

The churn limit quotient (65,536)

These variables are used to calculate the churn limit. This gives us the number of maximum validators that can exit the set every epoch.

Looking at the chart above, we currently stand at 502,933 validators. Over the past 30 days, there has been an average of 386 validators added per day. If we use this number and assume it stays relatively close ±386, we could possibly end up with nearly 530,000 validators. That puts us at a churn limit of 8, with the projected amount of 1800 validators who can exit per day.

It’s very hard to assume how many validators will want to exit, but let’s take some guesses. If we assume 1/3 of them want to exit, that’s 176,666 validators. That means it would take 98 days for them to all exit the queue. That is $8.47b USD of ETH pushing through a very tiny exit door, and it’ll take 3 months for them to all squeeze out. Despite this upgrade allowing lots of previous locked-away ETH to come online, everyone is curious to see where this ETH will flow. Are these people net sellers? Do they want to re-stake but in an LSD? Do they want to stake with Lido because they’ve proven themselves? Do they want the highest APR with Frax Finance? Do they want a centralized branded LSD with Coinbase?

Let's run a potential outcome if 1/3 of validators decide to exit:

Note: This is just my idea. Nobody…including myself can predict ETH flows post Shanghai

My thought process here was to chop these up into 3 categories.

Category 1: The Sellers

I assume 25% of validators exiting will want to sell. It’s hard to gauge the stakers who are up and who is underwater. ETH opened at $129 on Jan 1, 2020. Right before Beacon Chain went live, ETH closed at $575. 2020 ETH buyers could be up anywhere from 2-12x. If you were a buyer near the top, you could be down as bad as almost 70%. I would say it’s a healthy mix of both. Either way, people want liquidity and they are selling at the end of the day.

Category 2: The Unsure Bunch

This bunch isn’t 100% what they want to do yet. They ultimately decide by the time they get out of the queue, but it’s between selling and re-staking. I decided to split them evenly, and the re-stakers evenly spread their holdings across the 5 LSDs. That’s 180k ETH per LSD. The others end up selling their ETH.

Category 3: Re-Stakers

This category re-stakes their ETH immediately once they receive their ETH back. They think there is no better investment then ETH staking. They plan to hold for years to come and want to continue earning rewards.

This category ends up getting 2.8m of the ETH Flow.

33% flows to Lido (932k) as they’ve have proved themself as the largest LSD

25% flows to Frax (706k) as they’ve proved themself within many other DeFi products, offer the highest APR, and have a stellar team

25% flows to RocketPool (706k) as they’ve been a strong 2nd place for on-chain LSDs, and have made great progress on TVL

12.5% goes to Stakewise (353k). They offer the 2nd largest APR, but if you were looking at the best APR, you would choose Frax > Swise, and if not you would probably choose Lido

4.5% flows to Coinbase (127k). This feels small, but I feel like very few people who staked on-chain are going to send their ETH to Coinbase, stake for a lower APR and 2.5x the fee

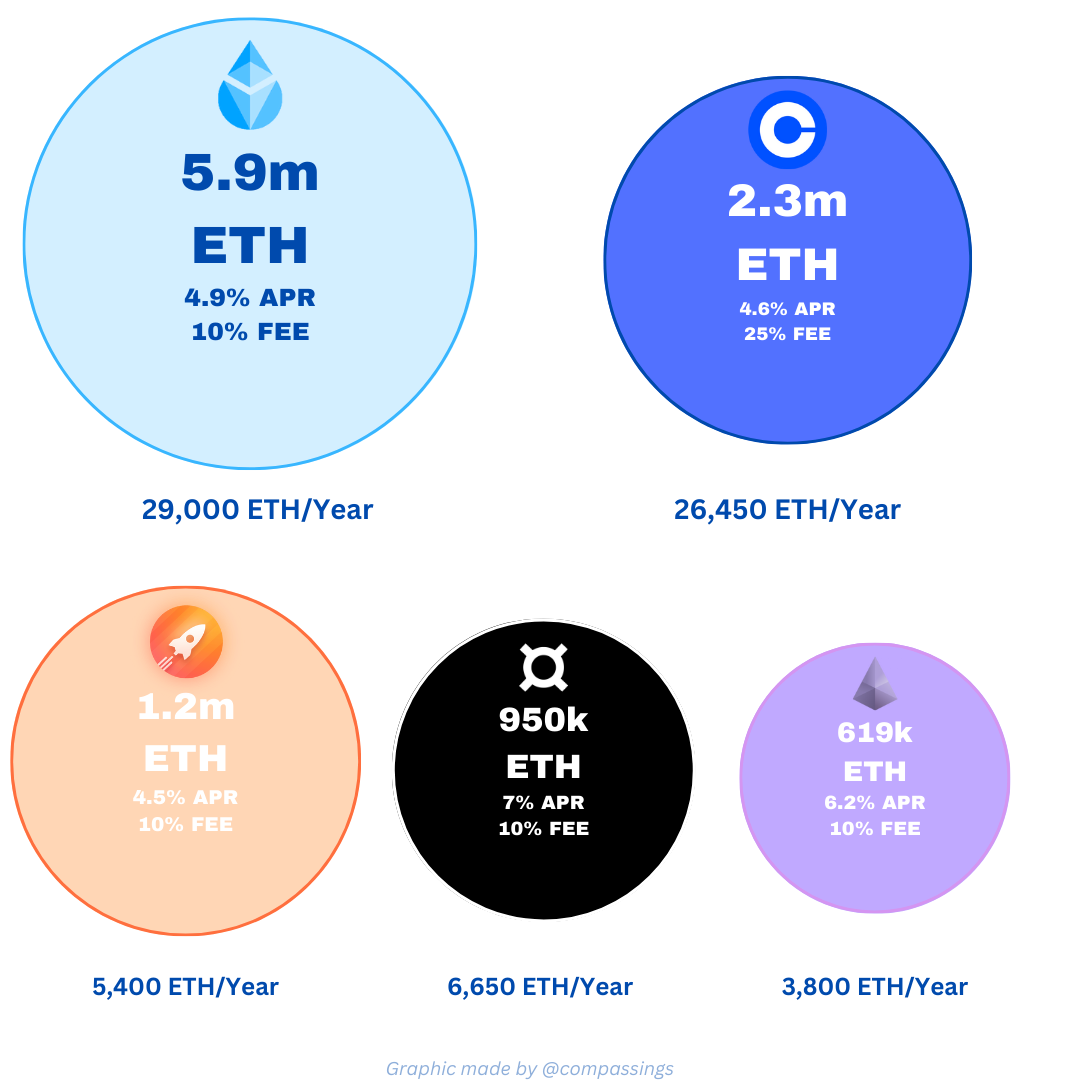

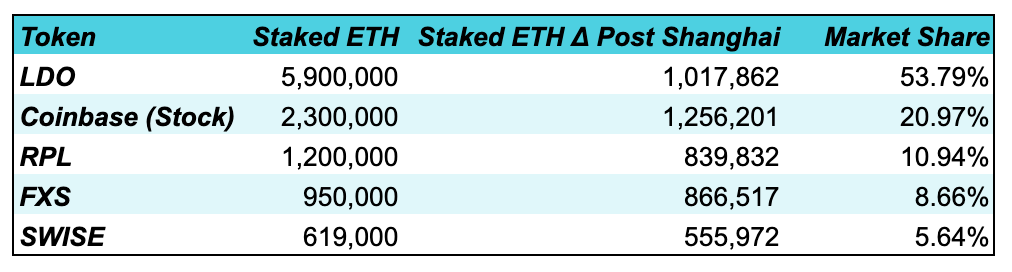

Post Shanghai, this is my idea of where these LSDs would stand. These are super rough estimates, but it’s interesting to speculate on potential growth and future fees generated.

This pushes Lido’s dominance down to around 50% from 73% across the DeFi LSDs. I assume Lido will always hold the #1 spot, but there will also be a healthy amount of competition. The only way I see them falling out of the #1 spot is if something bad were to happen (really hope not). This could be things like a large stETH → ETH price disparity like we saw in the summer of 2022 or maybe a governance change where they implement a new fee structure etc…I highly doubt they do that but you never know. The same thing applies to all LSDs. We will see how they operate under large ETH in-flows/out-flows and who is properly prepared for it.

Now, you may have noticed Coinbase only gained 300k ETH post-Shanghai in my chart but I added another 1m on the graphic above. This is because Coinbase has 1m legacy staked ETH that can be wrapped into cbETH. Eventually, all the legacy staked ETH→ cbETH and they’ll operate out of 1 bucket, not 2.

Despite Coinbase being 2nd place in the running, there’s a chance they generate a lot more fee’s then Lido does even if their TVL is lower. Coinbase charges 2.5x the fee that Lido does. It seems ridiculous, but it’s also incredibly easy for retail users to stake and earn. The average retail user who is interested in Crypto but doesn’t do anything on-chain is picking Coinbase staking 9 times out of 10. It takes two clicks and you are off to the races

Staking on a simple UI/UX for retail is way easier than starting a meta mask, writing down a seed phrase, connecting to a DApp, approving transactions, confirming transactions, and then making sure you don’t lose your crypto. It’s a long, confusing process for the average person and 95% of people don’t care to do so.

Coinbase currently custodies 18m ETH. If they market staking aggressively post Shanghai, they could easily see large in-flows into cbETH. The opportunity is sitting right in front of them to open up a major revenue driver. Last year, they saw trading revenue plummet and it hurt their balance sheet dramatically. cbETH can present an enormous non-trading revenue stream for them.

The highlighted grey area is where you want to focus. Those are modestly bullish assumptions on the revenue they can generate at those ETH prices relative to the cbETH they can amass over the coming months. Ultimately, it’s a no-brainer for them to push staking so they can be less reliant on trading revenue. The space is too volatile, and shareholders love diversified revenue streams.

Over the past few weeks, we’ve seen these coins perform extremely well. Lido is leading the way…up 136%. Frax ($FXS) is close behind them up 122%. I would expect the narrative of Liquid Staking Derivatives to be a major one for 2023. Shanghai is planned for late March and the exit queue will push us out to late June. Obviously, these are both reliant on a successful upgrade.

Thank you for reading! If you enjoyed my content feel free to subscribe below and follow me on Twitter @compassings.